The key to mitigate the impact of market uncertainty and to reduce potential losses caused by market volatility is to have a well-diversified portfolio aligned to long term investment objectives.

Investing in a range of different asset types with exposure to different sectors, countries, currencies will help to reduce the investment risk the portfolio is exposed to. This is because different asset classes generally react differently to certain market events. Nevertheless, designing an effective and efficient diversified portfolio can be seen as a complex and intimidating task especially in the current market environment of volatile equity markets and rising interest rates, where the conventional 60/40 portfolio construction is no longer an adequate foundation for solid investment returns.

Diversified portfolios can help to reduce risk in volatile times

To mitigate the impact of market volatility and to ensure long-term growth, a well-diversified portfolio must include a sufficient allocation of assets deemed defensive in nature or assets that do not move consistently in tandem with other holdings in a portfolio. These could be assets, such as structured products, which are designed to provide a level of capital protection or predefined outcomes. The key benefit of structured products is that they may provide pre-agreed returns in flat and sometimes even slightly declining market conditions while ensuring that investor’s capital is safeguarded, partially or fully, in the long term.

Combining differing types of structured products in a portfolio may help to ensure you receive defined results irrespective of the market conditions. For example, structured products that offer fixed returns, may help to maintain a flow of income over an agreed period (monthly, quarterly, etc), whereas participation notes can enhance the positive exposure to any underlying while keeping the capital partially or fully protected until the end of the investment term.

Ensuring the portfolio meets investors risk appetite

Like other investment vehicles, different structured products bear different levels of risk. It is important to ensure the structured products selected are aligned to the investors’ risk appetite and complement their wider portfolio.

Including structured products in the investment portfolio may help to optimise its overall risk/return ratio as they may offer not only capital protection but also stability and a level of certainty over potential future growth.

An important feature of structured products is that they enable the investors to remain exposed to equity market performance without significantly increasing the risk of their overall portfolio. This may help investors achieve their investment goals which may otherwise be unattainable. In other words, the investment goal may not be achievable with a balanced portfolio while an adventurous all equity portfolio may be too risky for the investor’s risk profile.

Let’s look at what this could look like in practise

Please note these examples are for illustration purposes only and not based on real market events. Structured products are capital at risk products, meaning whilst they may offer full or partial capital protection this is not guaranteed and is subject to the default risk of the issuer.

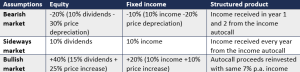

Product A – A 100% capital protected note, subject to issuer default risk, that offers investors 110% participation in the performance of an underlying equity index (for example FTSE 100) at the end of a 5-year term.

In five years’ time, the investor would expect to receive their capital back plus 110% of the upward performance of the FTSE 100, subject to issuer default risk. The growth received will not include any dividend payments as structured products use dividends to increase the participation and to finance the capital protection.

Product B – An income autocall note with a 5-year term that offers the investor a predefined return of 7% p.a. linked to performance of an underlying equity index (for example European stock index). The return is payable on the given observation dates if the underlying is at 85% or above of its initial level (this is known as a coupon barrier). The product B also has a 60% capital protection barrier; this means investors will receive all of their capital back unless the market has fallen by more than 40% at maturity. In such a situation the initial investment will be reduced on a one-to-one basis.

If in five years’ time, on the last observation date (assuming the 100% autocall barrier has not been breached on any of the previous observation dates), and the underlying equity index is not down by more than 15% compared to the initial level, the investor would expect to receive their capital back, as the capital protection barrier has not been breached, and a 7% p.a. (plus any previously missed coupons for each year invested; a total return of 35%), subject to issuer default risk.

‘The key difference of an income autocall and capital protected note is that the returns of income autocalls are more predictable than holding the underlying index fund while the capital protected product provides safety in market declines without a significant trade-off for the upside.’

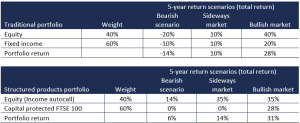

Now, let’s consider a traditional portfolio of 40% equities and 60% bonds in different market scenarios: bearish, sideways and bullish market. The assumptions are summarised in the table below. If we simplify and replace the assets in a traditional portfolio with structured products, we can compare how both portfolios perform. It is important to ensure that the investor’s portfolio is aligned to their risk appetite. Therefore, in this structured product portfolio example the equity allocation is replaced by an income autocall, and the bond allocation is replaced by a capital protected product. The autocall will provide a potential income and add equity risk to the portfolio while the capital protected note will provide a level of security and potential capital growth.

Source: Causeway Securities, for illustration purposes only.

5- year return comparison of a traditional portfolio and a portfolio of structured products

Source: Causeway Securities, for illustration purposes only

Source: Causeway Securities, for illustration purposes only

The above simplified example of replacing traditional assets in the portfolio with structured products, with a similar risk profile, shows that the structured products portfolio has the potential to outperform the traditional portfolio in every market scenario. The outperformance is most significant in the Bearish scenarios where the protection feature adds the most value to the portfolio.

While most wealth managers would not replace all traditional assets in the portfolio with structured products, the example demonstrates that the overall portfolio performance, especially during bearish market conditions, may be improved by including structured products in the portfolio.

‘The overall portfolio performance, especially during bearish market conditions, may be improved by including structured products the portfolio.’

Conclusion

Structured products may be a good tool to add diversification into a portfolio as they may provide a level of predictability to the portfolio returns and, due to the asymmetric payoff profiles, they can be less correlated to the traditional assets. This means that, if the markets are flat or falling, structured products may reduce the downside risks and improve the risk/return ratio of portfolios.

For more information about our structured products visit our Portal.

Important Information

This publication is intended to be Causeway Securities Limited own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell, or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price, or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice, you should contact your financial adviser.

Causeway Securities Limited is authorised and regulated by the Financial Conduct Authority. (FCA FRN 749440). Causeway Securities Limited is registered in England and Wales with company number 10102661. Registered address 2nd Floor 1 – 2 Broadgate Circle, London, England, EC2M 2QS.